Introduction

Since March 2017, Congress has debated several bills to repeal and replace the Affordable Care Act (ACA). Almost all the bills have included provisions to create a fund to provide billions of dollars for grants to states to stabilize their individual (non-group) health insurance markets and address cost and coverage issues. All three of the major bills considered by Congress also included amendments to simplify the application and approval process for Section 1332 of the ACA, titled Waiver for State Innovation, which allows states to waive certain provisions of the ACA and receive funding to implement new state-based programs and strategies to provide their citizens with access to affordable health care.

Two of the programs frequently suggested to address the cost of providing coverage for high-risk, high-cost individuals are traditional high-risk pools and reinsurance programs. This issue brief examines a small number of reports and limited summary data for 2000 through the first quarter of 2013 from the Kansas high-risk pool, which operated from 1994 through the end of 2013, and provided coverage for some Kansans at premium rates above the average market rate. KHI also has reviewed information about state-based reinsurance programs that have been implemented or proposed by other states, to describe the costs and benefits of these programs and how they impact a state’s individual health insurance market. To date, a total of seven states have implemented or proposed reinsurance programs.

Section 1332 of the ACA

While Congress has been considering repeal and replace legislation for the ACA, the Trump administration also has been encouraging states to consider using the existing Section 1332 provisions to address cost and coverage issues in their individual health insurance markets. On March 13, 2017, the U.S. Department of Health and Human Services (HHS) issued a letter to all state governors encouraging them to submit applications for waivers. Under existing Section 1332, states applying for waivers and funding must demonstrate that a proposed waiver will:

-

- Provide comprehensive coverage that is comparable to the coverage offered through the ACA;

- Ensure affordability by providing coverage and cost-sharing protection against excessive out-ofpocket spending;

- Provide coverage to at least a comparable number of residents as the ACA; and

- Ensure the waiver plan will not increase the federal deficit.

If a state’s approved waiver would make its eligible citizens and small businesses ineligible for the ACA’s premium tax credits, cost-sharing subsidies or small business tax credits, the state also may receive an aggregate amount of those unused funds to pay for marketplace coverage to implement the state’s waiver plan. The HHS letter specifically encouraged governors to consider implementing a high-risk pool or a state-operated reinsurance program to lower premiums, improve market stability and increase consumer choice in their health insurance markets. One state, Oregon, just received approval of its application in late October.

State-Operated High-Risk Pools

Under the ACA, insurance companies are prohibited from denying coverage to individuals with preexisting health conditions or setting premium rates based on health status. Prior to implementation of the ACA, individuals applying for coverage in the individual health insurance market with pre-existing health conditions were medically underwritten and subjected to pre-existing condition exclusions, charged higher premiums or denied coverage. Thirty-five states, including Kansas, operated traditional high-risk pools (in which enrollees were kept separate from the standard risk pool) prior to 2014 to provide state-based, subsidized health insurance coverage for individuals who were unable to obtain adequate and affordable coverage in the market.

Kansas’ Experience

K.S.A. 40-2117, et seq., the Kansas Uninsurable Health Insurance Plan Act, was passed by the Legislature in 1992 to establish a nonprofit legal entity known as the Kansas Health Insurance Association (KHIA). The Act requires all insurers providing health care benefits in the state to be members of KHIA, which operates under a plan established and exercised by a board of directors, with statutory oversight by the commissioner of insurance. For almost 20 years, until coverage was discontinued on January 1, 2014, KHIA operated a high-risk pool for Kansans who met certain eligibility requirements, including:

-

- Residing in Kansas for six months prior to application

- Having their health insurance coverage involuntarily terminated for any reason other than nonpayment of premium

- Having applied for health insurance and been rejected by two insurance carriers because of health conditions

- Being a child under the age of 19 who had been unable to purchase coverage under an individual health insurance policy because such coverage was not available for sale in the county in which they resided

- Having applied for health insurance and been quoted a premium rate in excess of the KHIA rate

- Having been accepted for health insurance subject to a permanent exclusion of a pre-existing disease or medical condition

- Meeting certain federal law requirements relating to having previous creditable coverage (generally recognized types of public and private insurance) that made them a “federally defined eligible individual.”

Resident dependents of persons who were eligible for KHIA coverage also were eligible for coverage.

Individuals who were not eligible for coverage included:

-

- Persons who were eligible for Medicare or Medicaid;

- Persons whose coverage with KHIA was terminated less than 12 months prior to the date of a current application (did not apply to federally defined eligible individuals);

- Persons who had received accumulated benefits from a KHIA plan equal to or in excess of the lifetime maximum benefits under the plan;

- Persons who had access to coverage through an employer-sponsored group or self-insured plan; or

- Persons who were eligible for any other public or private program that provided health services.

A third-party administrator selected by the board was responsible for collecting premiums, processing the payment of claims, and submitting quarterly reports to the board regarding the operation of the pool. The board was responsible for setting premiums and setting and collecting assessments on the KHIA member insurance companies in proportion to their annual respective market shares of total health premiums received in the state to cover the net losses experienced by KHIA.

Enrollment

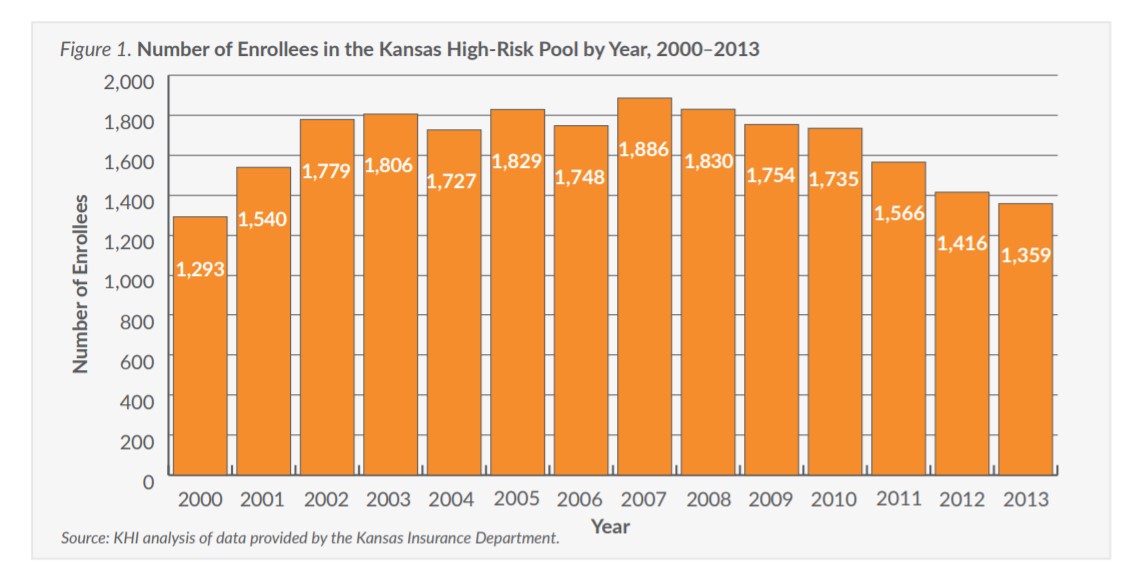

In 1994, the first year of operation for the Kansas high-risk pool, KHIA had 578 enrollees. Enrollment continued to grow into the mid-2000s (Figure 1), peaking at 1,886 in 2007, and then tapering off through 2013, with 1,359 enrolled in the last year of operation.

With full implementation of the health insurance provisions of the ACA in 2014, KHIA enrollees were able to purchase guaranteed-issue insurance coverage on or off the federally facilitated marketplace, and enrollment in the KHIA plan was terminated effective January 1, 2014.